Admission of a partner in a partnership firm refers to the process of adding a new member to the partnership. When a new partner is admitted to the partnership, they become jointly and severally liable for the partnership's debts and obligations. This means that each individual partner is responsible for the entire amount of the partnership's debts and obligations, not just their share.

The process of admitting a new partner to a partnership can vary depending on the specific terms of the partnership agreement and the laws of the jurisdiction in which the partnership is located. In India, the provisions of Indian Partnership Act, 1932 are followed. In general, however, the following steps may be involved in admitting a new partner:

- Negotiating the terms of the new partnership: The existing partners and the prospective new partner should discuss and agree on the terms of the new partnership, including the new partner's share of the profits and losses, their duties and responsibilities, and any other relevant terms.

- Drafting a written agreement: It is a good idea to document the terms of the new partnership in a written agreement, which should be signed by all parties. This can help to avoid misunderstandings and conflicts in the future. However having a written agreement is not mandatory.

- Registering the new partnership: If the partnership is required to register with the government or any other regulatory body, the new partnership will need to be registered with the appropriate authority. In India registering a partnership is not compulsory and it is optional.

Preconditions for admission of a partner

a) If it is agreed in the partnership deed and b) in the absence of a partnership deed if it is agreed by all the partners. So a new partner cannot be admitted unless consent is given to this by all the existing partners.

Rights and Liabilities of a new partner

- Has the right to share of future profits as per profit share as agreed

- Has the right to share the assets of the firm

- Becomes liable for the losses incurred or the liabilities incurred after his admission

- Since the new partner gets the share in profits/assets which comes from the share of existing partners , it means that the existing partners are sacrificing their share. So to compensate them for this sacrifice, the new partner pays them in the form of Goodwill

- New partner has to bring in capital in the partnership firm as agreed

Effects of admission of a partner

- In future the partners will share the profits in the new profit sharing ratio

- New partner brings the amount of capital and Goodwill as agreed mutually

- New partner gets the right to share in assets of the firm and becomes liable to its liabilities

- Assets and Liabilities of the firm are revalued as on date

- Old partnership comes to an end and a new partnership comes into existence

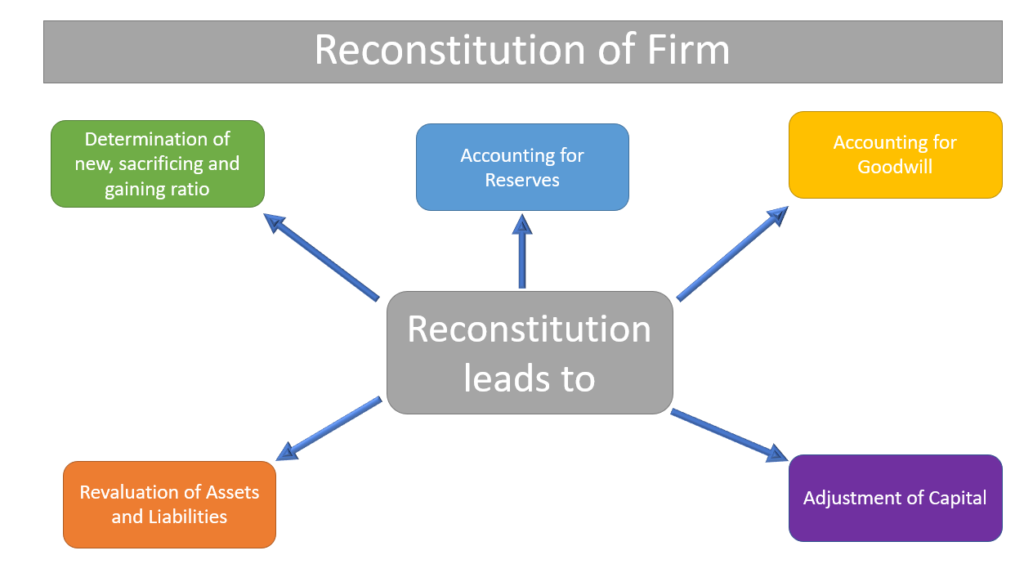

Adjustments required on admission of a new partner

Admission of a new partner is basically the reconstitution of a firm. So the adjustments done at the reconstitution of a firm are also done at the admission of a new partner and are as follows :

- Determining new ratio of all partners and gaining/sacrificing ratio for existing partners

- Valuation and adjustment for Goodwill

- Revaluation of assets and Liabilities and its adjustment

- Adjustment for reserves, accumulated profits and losses

- Adjustment of capital